Don’t Fear the Reaper: How to Save Social Security

“The Old-Age and Survivors Insurance (OASI) Trust Fund will be able to pay 100 percent of total scheduled benefits until 2033.. At that time, the fund’s reserves will become depleted and continuing program income [payroll tax] will be sufficient to pay 77 percent of total scheduled benefits,” according to the 2025 Social Security Trust Report.

As I near retirement after paying 12.4% (employer and employee combined payroll tax) of my salary for four decades, the last thing I want is to receive only 77% of scheduled benefits starting in 2033 - damn right, it’s personal!

Impact of baby boomers retiring

The OASDI Trust Fund is $2.5 trillion at the end of 2024, accumulated from decades of baby boomers paying into the fund from payroll taxes exceeding the benefits paid to past retirees. Now that baby boomers are retiring, however, Social Security paid out $1.3 trillion to 68 million retirees in 2024, which exceeded the $1.2 trillion of payroll tax income from current workers, and drawing on the trust fund by $104 billion in 2024.

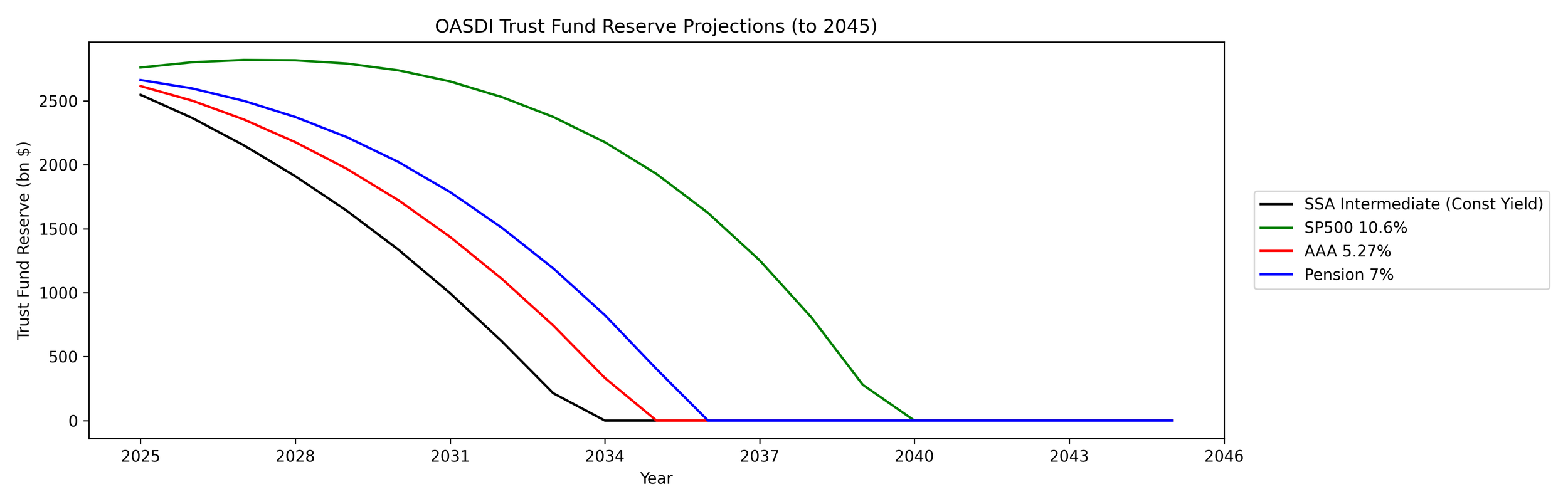

Problem: Trust Fund invests in U.S. Treasury bonds earning only 2.50%

Social Security does not run out of money if the Trust Fund runs out, as current workers payroll taxes fund benefits for retirees. However, due to the number of baby boomers retiring, only 2 workers pay for each retiree’s benefits. This shortfall, $104 billion in 2024, is paid by the Trust Fund which is the surplus that grew while baby boomers were working. In addition, Social Security benefits increase by the Consumer Price Index for inflation, which is projected rising at 2.4% per year. The 2.50% return on the $2.5 trillion Trust Fund is not adequate to fund the shortfall between payroll tax income and Social Security benefits paid out.

Solution: S&P500 portfolio would extend Trust Fund to 2040

The funding gap between payroll taxes and Social Security benefits rises from $209 billion in 2025 to $442 billion in 2032. The OASDI Trust Fund must fully invest in large cap stocks like most pension funds, rather than US Treasury securities, to extend the Trust Fund. Corporate AAA-rated bonds yield 5.27%. CalPERS, the California Public Employees Retirement System, has a 7.00% target return managed by a panel of investment advisors. Public pension funds and most well-managed 401(k) accounts achieve 6-7% returns from well-diversified equity mutual funds and ETFs.

ChatGPT analysis of 2005 Social Security Trust Report

IMHO, equity risk is now required to delay depletion of the reserve. The S&P500 index annual return of 10.6% since 2005 (included 2009 Great Recession crash) would delay Trust Fund depletion until 2040. Some call this idea “privatizing” social security, but that’s a misnomer since public employee pension funds like CalPERS are managed this way.

ChatGPT-created spreadsheet model using 2025 Trust Fund Report assumptions with interest rate as variable.

Why seek equity risk for an extra 6 years?

I’d much prefer if social security benefits weren’t cut until I’m 79 when my expenses are lower, rather than at 74! By 2040, most baby boomers will reach average life expectancy so its demographic bulge will return to fewer retirees.

Finally, the projections underscore it would be better to make program changes sooner rather than later, so the Trust Fund could earn S&P returns to extend past 2040.